How Silicon Valley Bank Collapsed | Explained

On Friday, Silicon Valley Bank abruptly failed. Speculators are worried that its failure could set off a domino effect in the banking industry.

Although the US government has intervened to protect depositors, SVB’s demise has repercussions in international financial markets. Signature Bank, a regional bank on the verge of failure, was closed by the government, who also insured the bank’s deposits.

On Monday, US Vice President Joseph Biden assured Americans that “our financial system is safe” and that “we will do whatever is needed on top of all this” as a sign of how seriously officials are treating the SVB debacle. The largest American bank failure since the 2008 financial crisis is described here.

What is Silicon Valley Bank?

Until it failed in 2016, Silicon Valley Bank, which had been around since 1983, was the 16th largest commercial bank in the United States. About half of all technology and life science startups in the United States that received funding from venture capitalists used its banking services.

Canada, China, Denmark, Germany, Ireland, Israel, Sweden, and the United Kingdom are all places where it operates. SVB reaped enormous rewards from the IT industry’s meteoric rise in recent years, which was propelled by record-low borrowing rates and a surge in demand for digital services in the wake of a global epidemic.

Bank assets (which include loans) more than quadrupled between the end of 2019 and the end of March 2022, reaching a peak of $220 billion. Thousands more tech firms parked their cash at the lender, increasing the total amount deposited from $62 billion to $198 billion over that time period. The company more than doubled the size of its global workforce.

Why did SVB Collapse?

In a classic run on the bank, customers withdrew their money from SVB over the course of 48 hours, leading to the bank’s unexpected demise. But, its collapse has been in the works for quite some time. SVB invested billions of dollars in US government bonds during the period of near-zero interest rates, as did many other banks.

The Federal Reserve aggressively increased interest rates in an effort to curb inflation, and what had appeared like a safe bet quickly unraveled. Rising interest rates reduce the value of bond holdings, hence the sudden increase in rates was detrimental to SVB’s bond holdings. Last week, the portfolio was reportedly yielding an average of 1.79%, which was significantly lower than the yield on 10-year Treasuries (about 3.9%).

As a result, tech startups had to allocate more capital toward debt repayment as a direct result of the Fed’s hiking spree, which increased the cost of borrowing money. They were also having trouble attracting additional venture finance.

The result was that businesses had to dip into their deposits at SVB to keep running and expand.

Why did the Bank Run Occur?

The bank run began on Wednesday after SVB stated it had sold a number of securities at a loss and would sell $2.25 billion in new shares to patch the hole in its finances. The troubles at SVB may be traced back to the bank’s prior investment decisions.

Many consumers panicked and withdrew all their cash at once. For investors worried about a replay of the global financial crisis of 15 years ago, the bank’s stock dropped 60% on Thursday, bringing down the value of other bank shares.

Trading in SVB shares was halted on Friday morning, and the company gave up on its attempts to raise funds or find a buyer. Since the bank was closed and placed in receivership by California regulators under the FDIC, its assets will be liquidated to repay depositors and creditors.

How about Investors and Depositors?

On Sunday, US authorities assured SVB customers that their money was safe with them. This action is being taken to help computer companies avoid further bank runs and ensure that they can keep paying their employees and operating expenses.

However, shareholders and bondholders will not be safeguarded because the intervention is not a bailout in the vein of the one implemented in 2008.

“Let me be clear that there were investors and owners of systemic major banks who were bailed out during the financial crisis… Treasury Secretary Janet Yellen said as much to CBS on Sunday, “we’re not going to do that again” due to changes put in place.

Nonetheless, “we are focused on attempting to address the needs of depositors.”

Will this Cause a Financial Crisis?

Now, other banks are showing indications of strain. On Monday, shares of First Republic Bank (FRC) and PacWest Bancorp (PACW) fell 65% and 52%, respectively, prompting a temporary halt in trading for both companies. Around 11.30 a.m. ET on Monday, shares of Charles Schwab (SCHW) were down 7%.

The Stoxx Europe 600 Banks index slumped 5.6% during European morning session, marking its worst drop since March 2018. This index follows 42 major EU and UK banks. The Credit Suisse share price dropped by 9% as the Swiss banking giant continued to face scandal.

The value of financial institutions’ investments in government bonds and other assets is down significantly, and SVB is no exception. US banks had $620 billion in unrealized losses at the end of 2022, the FDIC reports. These losses are the result of assets that have declined in value but have not yet been sold.

The Fed announced on Sunday that it would make additional cash available for qualifying financial institutions to avoid the next SVB from collapsing, a warning that regulators are worried about widespread financial upheaval.

The majority of experts agree that safety nets at banks in the United States and Europe are significantly more robust now than they were before the 2008 financial crisis. In addition, they stress that SVB’s exposure to the technology industry, which has been struck particularly hard by rising interest rates, was excessively high.

Researchers David Covey, Adrian Cighi, and Jaimin Shah from M&G Investments wrote in a blog post on Monday that while SVB is a big failure, it and other specialist companies like Signature are quite distinctive in the broader banking sector. As a result of its singularity, “it is unlikely to produce material problems for any of the great diversified banks in the US or Europe from a credit point of view,” the authors write.

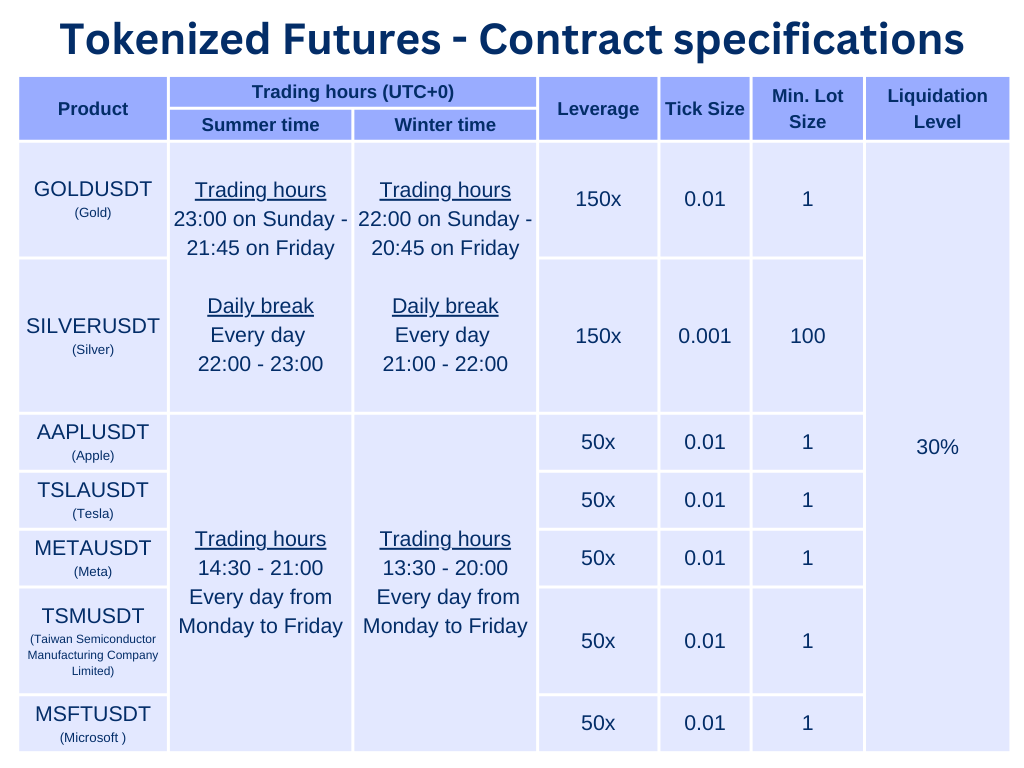

Where to Trade Tokenized Futures?

BTCC have also launched tokenized stock and commodity USDT-margined futures. Now you can trade gold, silver and stock on BTCC. These tokenized futures contracts are innovative products invented by BTCC, and users can trade stocks and commodities with USDT on our platform. Below are the details of the newly-added trading pairs.

BTCC offers exclusive bonus for new users. Sign up and deposit on BTCC to get up to 3,500 USDT in bonuses. Meet the deposit targets within 30 days after successful registration at BTCC, and you can enjoy the bonus of the corresponding target levels. Find out what campaigns are available now: https://www.btcc.com/en-US/promotions

iOS QR Code Android QR Code

Why Trade Tokenized Futures on BTCC

To trade tokenized futures, you can choose BTCC crypto exchange.BTCC, a cryptocurrency exchange situated in Europe, was founded in June 2011 with the goal of making crypto trading reliable and accessible to everyone. Over 11 years of providing crypto futures trading services. 0 security incidents. Market-leading liquidity.

Traders may opt to trade on BTCC for a variety of reasons

- Secure:safe and secure operating history of 11 years. Safeguarding users’ assets with multi-risk management through the ups and downs of many market cycles

- Top Liquidity:With BTCC’s market-leading liquidity, users can place orders of any amount—whSHIBer it’s as small as 0.01 BTC or as large as 50 BTC—instantly on our platform.

- Innovative:Trade a wide variety of derivative products including perpetual futures and tokenized USDT-margined stocks and commodities futures, which are innovative products invented by BTCC.

- Flexible:Select your desired leverage from 1x to 150x. Go long or short on your favourite products with the leverage you want.

BTCC FAQs

1.Is BTCC safe?

Since its inception in 2011, BTCC has made it a priority to create a secure space for all of its visitors. Measures consist of things like a robust verification process, two-factor authentication, etc. It is considered one of the most secure markets to buy and sell cryptocurrencies and other digital assets.

2.Is it possible for me to invest in BTCC?

Users are encouraged to check if the exchange delivers to their area. Investors in BTCC must be able to deal in US dollars.

3.Can I Trade BTCC in the U.S?

Yes, US-based investors can begin trading on BTCC and access the thriving crypto asset secondary market to buy, sell, and trade cryptocurrencies.

BTCC Guide-How to Deposit Crypto on BTCC?

What is Leverage in Cryptocurrency? How Can I Trade at 100X Leverage?

Best Crypto Exchange to Trade with Leverage

Best High Leverage Crypto Trading Exchange Platform

ADA Cardano Price Prediction 2025, 2030

Algorand Price Prediction 2030

MANA Coin Price Prediction 2030

HBAR Price Prediction 2022, 2025, 2030

Stellar Lumens (XLM) Price Prediction 2030

Algorand (ALGO) Price Prediction 2022, 2025, 2030

Apecoin Price Prediction 2022, 2025, 2030

CRO Crypto Price Prediction 2025

XRP Price Prediction 2022, 2025, 2030

Solana (SOL) Price Prediction 2022,2050, 2030

Ethereum Price Prediction 2022, 2025, 2030

Avalanche (AVAX) Price Prediction 2022,2025,2030 – Is AVAX a Good Investment?

Chainlink (LINK) Price Prediction 2023, 2025, 2030 – Is LINK a Good Investment?

Dogecoin (DOGE) Price Prediction 2023, 2025, 2030 – Will DOGE Explode in 2023?

Bitcoin (BTC) Price Prediction 2023, 2025, 2030 – Is BTC a Good Investment?

Litecoin Price Prediction 2023, 2025, 2030: Is Litecoin a Good Investment?

Dash Price Prediction 2023, 2025, 2030: Is DASH a Good Investment?

GMT Price Prediction 2023, 2025, 2030: Is GMT Coin a Good Investment?

Bitcoin Cash Price Prediction 2023, 2025 and 2030: Is Bitcoin Cash a Good Buy?

Yearn.Finance (YFI) Price Prediction 2023, 2025, 2030 – Is YFI a Good Investment

Bitcoin SV Price Prediction 2023, 2025, 2030: Is Bitcoin SV a Good Investment?

Tron (TRX) Price Prediction 2023, 2025, 2030 — Will Tron Hit $1?

Gala (GALA) Price Prediction 2023, 2025, 2030 — Is GALA a Good Investment?

Blur Price Prediction 2023, 2025, 2030: Is Blur Crypto a Good Investment?

Fantom (FTM) Price Prediction 2023, 2025, 2030—Is FTM a Good Investment?

Polkadot (DOT) Price Prediction 2025 – 2030: Is Polkadot a Good Investment?

Aptos (APT) Price Prediction 2023, 2025, 2030- Will APT Go Up?

Bitcoin SV Price Prediction 2023, 2025, 2030: Is Bitcoin SV a Good Investment?

Aptos (APT) Price Prediction 2023, 2025, 2030- Will APT Go Up?