Alphabet’s TPUs: The $900 Billion Chip Disruption Wall Street Didn’t See Coming

Google's parent company just revealed its secret weapon—and it's aimed squarely at the heart of the semiconductor industry.

Not Your Average Chip

Alphabet's Tensor Processing Units, or TPUs, were once just an internal tool to power its own AI ambitions. Now, they're emerging as a potential market-shaking force. The math is staggering: a business line that could be worth nearly a trillion dollars. That's not a typo. It's a number that makes even the most seasoned chip veterans do a double-take.

Why This Changes Everything

Traditional chipmakers have operated in a cozy world of predictable upgrade cycles and loyal customers. Alphabet's move cuts through that complacency. It bypasses the entire legacy supply chain, proving that the biggest player in AI doesn't need to wait in line for someone else's silicon. They're building their own—and it's better, faster, and purpose-built for the AI era.

The Domino Effect

This isn't just about selling chips. It's about control. By owning the core hardware that runs its massive AI models, Alphabet locks in performance advantages and cost efficiencies that competitors can't match. It turns cloud computing into a vertically integrated powerhouse, where every layer of the stack—from software to silicon—is optimized in-house. Analysts scrambling to update their models look like they're using abacuses.

A Trillion-Dollar Warning Shot

The $900 billion figure isn't a revenue projection; it's a valuation of the strategic moat being built. It represents the future value of an AI ecosystem untethered from third-party hardware constraints. For the old guard, it's a brutal reminder that in the tech arms race, the company that controls the foundational technology controls the kingdom. Wall Street, meanwhile, is probably still trying to figure out if a TPU is a new kind of stock ticker.

The chip game has new rules. Alphabet just wrote them.

Read us on Google News

Read us on Google News

In brief

- Alphabet’s TPUs drive a 31% Q4 rally as investors bet on new revenue from external chip sales and rising demand for AI hardware.

- Major firms like Anthropic and Meta show interest in Alphabet’s chips, pushing market confidence and expanding growth expectations.

- TPU design offers a cheaper alternative to Nvidia hardware, drawing attention as companies look for more cost-effective AI solutions.

- Despite a higher valuation, investors see further upside as Alphabet strengthens its chip strategy and advances its cloud performance.

TPUs Drive 31% Q4 Surge as Investors Bet on New Chip Revenue

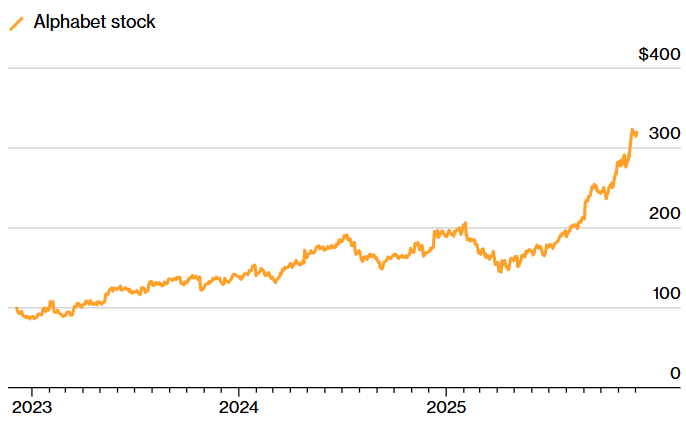

Alphabet’s TPUs are playing a major role in the company’s strong fourth-quarter rally. Shares are up 31%, putting the stock among the best performers in the S&P 500. Internally, TPUs have supported Google Cloud’s growth for years by handling large-scale machine-learning tasks. Now investors think Alphabet may start selling the chips to outside customers, creating a new long-term revenue path.

Confidence has grown as forecasts point to the possibility of large-scale external sales. Gil Luria of DA Davidson explained that TPUs could appeal to companies seeking alternatives to Nvidia, giving Alphabet a path into an expanding market.

He estimates that Alphabet could capture roughly 20% of the AI-chip segment over several years, a business he values at about $900 billion. Even without external chip sales, improved performance within Google Cloud strengthens the company’s position.

Nvidia, which remains the leading supplier of high-end AI hardware, responded indirectly. A spokesperson pointed to CEO Jensen Huang’s recent comments, noting that only a small number of teams worldwide can produce such complex products. According to the spokesperson, Nvidia views its engineering capabilities as a lasting advantage.

Investor interest in Alphabet’s chips accelerated throughout the fall. In late October, reports surfaced that the company WOULD supply tens of billions of dollars’ worth of TPUs to Anthropic. And as a result, this led to a two-day stock jump of more than 6%.

About a month later, new reports suggested that Meta was considering a multibillion-dollar investment to gain access to the chips, contributing to another market uptick.

Alphabet Chips Draw Attention as Nvidia Costs Climb

TPUs take a different approach from Nvidia’s general-purpose chips. Built as application-specific circuits, they focus on running machine-learning tasks with high throughput and reduced costs.

And while they don’t offer the same flexibility as Nvidia hardware, these chips provide a cheaper option at a time when investors are closely monitoring AI expenses.

Mark Iong of Homestead Advisers says Nvidia’s chips remain costly and hard to get. In turn, Alphabet’s ASIC design could draw buyers willing to adjust their workloads to fit the cheaper option.

Nvidia chips are much more costly and hard to get, but if you can use an ASIC chip, Alphabet is right there, and it leads that market by far. It won’t control the entire market, but this is part of the secret sauce for the stock.

Mark IongA combination of market conditions and product developments is shaping sentiment:

- Growing demand for more affordable AI-focused hardware.

- Alphabet’s ability to scale its TPU program.

- Interest from large buyers such as Anthropic and Meta.

- Limited supply and high cost of Nvidia equipment.

- Wider internal use of TPUs within Google Cloud services.

The company’s latest Gemini model added further support. Gemini was built to run efficiently on TPUs, reinforcing the hardware’s importance within Alphabet’s broader product lineup.

Portfolio Managers Trim Alphabet but Maintain Confidence in AI Roadmap

Despite rising expectations, valuation remains a point of discussion. Shares now trade at a price-to-earnings ratio of 27, the highest since 2021 and above the long-term average. Even so, the stock is still cheaper than major peers, including Apple, Microsoft, and Broadcom.

Some investors trimmed positions during the rally. Allen Bond of Jensen Investment Management reduced his holdings as the stock climbed, but still sees room for further gains. He considers the company’s overall position solid and views current pricing as reasonable relative to expectations.

Bond also says that progress in AI across Alphabet supports the possibility of future revenue from TPUs, even if adoption takes time. With the company trading at a discount to leading rivals and showing fast advancement in chip development, he continues to hold Alphabet as a Core position.

Maximize your Cointribune experience with our "Read to Earn" program! For every article you read, earn points and access exclusive rewards. Sign up now and start earning benefits.